Vietnam’s tax landscape continues to evolve rapidly in 2026 to support economic growth while aligning with international standards (BEPS 2.0, OECD, and CPTPP commitments). In February 2026, the Vietnamese Government issued several key decrees and circulars that introduce important changes to Value Added Tax (VAT), Corporate Income Tax (CIT), Personal Income Tax (PIT), and tax administration procedures. These updates directly impact foreign-invested enterprises (FDI companies), profit repatriation, compliance costs, and cash flow planning.

This article provides a clear, practical summary of the most relevant February 2026 tax updates for foreign investors and FDI companies operating in Vietnam.

1. Major VAT Updates Effective from 2026

- VAT Rate Structure Remains Stable: Standard rate stays at 10%. Reduced rate of 5% and 0% continue to apply to priority sectors.

- New VAT Refund Mechanism for FDI Projects (Decree 12/2026/ND-CP):

Foreign investors in encouraged sectors (high-tech, semiconductor, renewable energy, and R&D) can now apply for automatic VAT refund on investment phase inputs within 30 working days instead of the previous 60–90 days. This significantly improves cash flow for large manufacturing and infrastructure projects. - Tighter Rules on VAT for E-commerce and Digital Services: Foreign providers of digital services (software, streaming, online advertising) to Vietnamese customers must continue charging 10% VAT via the direct registration portal. New penalties for non-compliance increased up to 3x the unpaid tax.

- Expanded VAT Exemption List: Certain green technology equipment and components for solar/wind power projects are now fully exempt from VAT until the end of 2030.

Practical Tip for FDI: Ensure your company correctly classifies input VAT on fixed asset purchases and construction materials — the new fast-track refund process only applies if documentation is submitted electronically via the General Department of Taxation portal.

2. Corporate Income Tax (CIT) Updates 2026

- Standard CIT Rate: Remains 20%.

- Preferential CIT Rates Extended and Clarified:

- 10% for 15 years (extendable) for projects in high-tech zones, innovation centers, and semiconductor manufacturing.

- 15% for 10 years for large-scale agricultural processing and renewable energy projects.

- New 17% rate for certain R&D companies meeting specific expenditure thresholds.

- Minimum Tax Rule (Pillar Two – BEPS 2.0): Effective from 1 January 2026, large multinational groups with global revenue over €750 million must pay a minimum effective tax rate of 15%. Top-up tax will be collected in Vietnam if the effective rate is lower.

- Deductible Expenses Tightened: Entertainment, dining, and certain related-party transactions now face stricter documentation requirements. Interest expense deduction cap remains at 30% of EBITDA for thin capitalization rules.

Important for FDI: The new February guidance clarifies how to calculate the “encouraged investment” CIT exemption period — it now starts from the year the project generates revenue, not from the first year of operation.

3. Personal Income Tax (PIT) Changes in February 2026

- Tax Residency Rule Clarified: Individuals staying in Vietnam 183 days or more in a calendar year (or having a permanent residence) are considered tax residents, subject to progressive PIT rates on worldwide income.

- Progressive Tax Rates Unchanged (5% to 35%).

- New Tax Relief for Expatriates:

- Housing allowance and school fees for children of foreign employees are now fully exempt from PIT if properly documented (up to certain reasonable limits).

- Stock options and long-term incentives granted to key personnel in FDI companies receive deferred taxation until realization.

- Withholding Tax on Dividends and Interest: Remains at 5% for dividends paid to foreign corporate shareholders (under most DTAs) and 5–10% for interest.

Recommendation: Foreign employees and expats should carefully track days of presence in Vietnam, especially with the rise of hybrid working arrangements.

4. Tax Administration & Compliance Reforms (February 2026)

- Full Digital Transformation: All tax declarations, payments, and invoices must be submitted electronically. Paper-based filings are no longer accepted for FDI enterprises from March 2026.

- New Risk-Based Audit System: The General Department of Taxation introduced an AI-supported risk scoring model. Companies in conditional sectors, large related-party transactions, or claiming high incentives are more likely to be audited.

- Extended Deadline for Annual Finalization: Corporate income tax finalization deadline extended to 90 days after the fiscal year-end for companies with foreign investment.

- Stronger Anti-Avoidance Measures: New rules on beneficial ownership and substance-over-form tests for claiming tax treaty benefits (especially with Singapore, Hong Kong, and UAE).

- Penalties Increased: Late payment interest remains 0.03%/day, but administrative fines for transfer pricing violations and incorrect incentive claims have increased significantly.

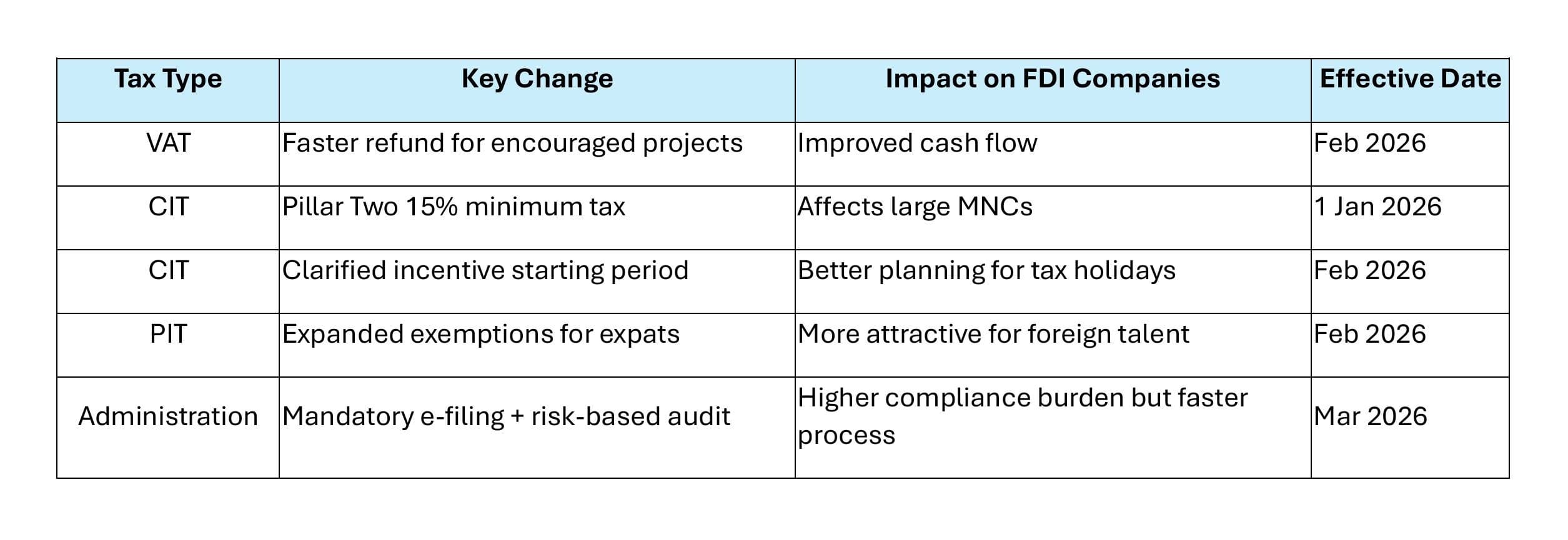

Summary Table: Key Tax Updates February 2026

Action Points for Foreign Investors in 2026

- Review your current tax incentive certificates and apply for adjustments under the new guidance.

- Update transfer pricing documentation before the 2026 finalization deadline.

- Implement robust VAT input credit tracking systems.

- Reassess expatriate compensation packages to maximize PIT exemptions.

The information provided in this article is for general informational and reference purposes only. It reflects the legal and tax framework as of February 2026 and does not constitute official legal or tax advice. Tax laws in Vietnam are complex and subject to interpretation and change.

We strongly recommend that you consult our experienced FDI tax lawyers and qualified tax advisors for a detailed assessment, compliance review, and tailored solutions that best suit your specific business situation and investment project.

Read more other relavant articles:

- FDI Enterprises and the Private Sector Question: An Emerging Interpretative Risk in Vietnam’s Tax Incentive Framework

- Tax Obligations and Incentives for FDI Companies in Vietnam

- Understanding Taxation and Legal Obligations for Expats in Vietnam

- 7 Key Points to Prevent Tax Disputes

- Business Structures for Foreign Investors in Vietnam: Complete 2026 Guide – LLC, JSC, Branch, Representative Office & More