A Policy Milestone – But More Than Procedural Reform

On 31 March 2026, the Government promulgated Decree 103/2026/ND-CP, providing detailed guidance on outbound investment under the Law on Investment 2025. At first glance, the Decree appears to be a continuation of administrative reform, aimed at facilitating Vietnamese investors’ expansion abroad in an increasingly integrated global economy.

However, at a deeper level, Decree 103 is far more than a technical implementing instrument. It reflects a structural shift in regulatory philosophy: from controlling whether investors are allowed to go abroad, to controlling how capital behaves once it has left the country.

In other words, the State is no longer primarily guarding the “front gate” of approval, but is instead supervising the entire lifecycle of outbound investment capital.

Conditional Liberalisation: The Retreat of Front-End Control

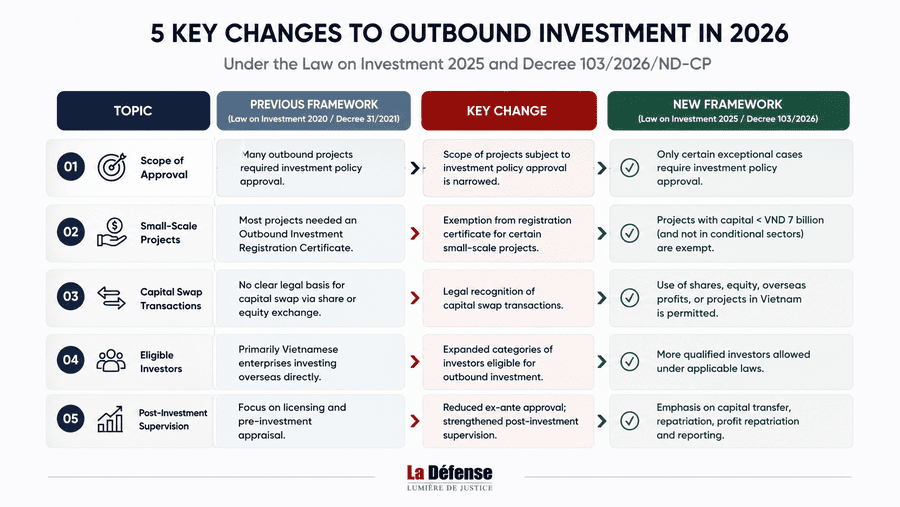

One of the most notable features of Decree 103 is the relative relaxation of ex-ante approval mechanisms. Conditions for outbound investment are now more clearly defined and transparent, without being overtly restrictive.

In principle, investors are afforded greater room to undertake overseas investments, provided that they can demonstrate:

- Financial capacity

- Legitimacy of capital sources

- Feasibility of the investment project

Yet, this liberalisation does not equate to deregulation. On the contrary, it is accompanied by a more sophisticated and pervasive layer of control.

That layer is capital control.

Capital Control as the Core Regulatory Logic

At its core, Decree 103 places outbound investment capital within a tightly monitored framework.

Key regulatory areas include:

- Capital accounts for outbound investment

- Cross-border capital transfers

- Profit repatriation

- Capital recovery mechanisms

These are closely aligned with foreign exchange regulations and anti-money laundering frameworks.

The policy message is clear: the State is less concerned with where investors choose to invest, and more concerned with whether the capital flows are transparent, traceable, and ultimately beneficial to the domestic economy.

This approach is consistent with international regulatory trends. However, it also introduces significant practical challenges.

Practical Challenges: When Ex-Post Control Becomes the New Bottleneck

From a practitioner’s perspective, several implementation challenges are already foreseeable.

First, regulatory fragmentation. Outbound investment is not governed solely by investment law, but intersects with banking, foreign exchange, and tax regulations. Divergent interpretations among authorities may result in situations where transactions are legally compliant yet practically unworkable.

Second, the burden of proving lawful capital sources. While conceptually sound, this requirement can be difficult to satisfy for many Vietnamese investors—particularly SMEs and those employing multi-layered investment structures.

Third, reporting obligations. Ex-post supervision relies heavily on reporting systems. Yet, current reporting mechanisms remain largely manual, fragmented, and insufficiently digitalised. This risks turning compliance into an administrative burden rather than an effective regulatory tool.

Policy Gaps: Unresolved Structural Issues

Despite its advancements, Decree 103 leaves several critical issues unaddressed.

First, the absence of a unified framework for indirect outbound investment. While portfolio investments and fund-based investments are excluded from the Decree’s scope, this exclusion highlights the fragmentation between investment law, securities law, and foreign exchange regulations. Investors are effectively left navigating these regimes without clear coordination.

Second, the lack of guidance on complex investment structures. Multi-tier structures involving intermediary jurisdictions such as Singapore or Hong Kong are standard in practice. However, the Decree does not clarify how such structures should be treated from a regulatory or reporting perspective.

Third, insufficient integration with tax and transfer pricing regulations. Outbound investment is inherently linked to profit allocation, related-party transactions, and BEPS considerations. Yet, Decree 103 does not meaningfully address these dimensions, leaving a significant regulatory gap.

Fourth, limited attention to investor protection abroad. While the Decree establishes robust control mechanisms, it provides little in terms of legal protection or support for Vietnamese investors operating overseas.

A Policy Paradox: More Open, Yet More Demanding

Decree 103 presents an interesting paradox.

At the policy level, the outbound investment regime is more open, transparent, and aligned with international practices.

At the implementation level, however, compliance has become more complex. Investors must now navigate not only investment law, but also foreign exchange, tax, financial structuring, and international legal frameworks.

In essence, the door is wider open—but the path beyond it requires significantly greater sophistication.

Strategic Perspective: A Selective Regulatory Framework

From a strategic standpoint, Decree 103 appears to serve a filtering function.

Investors who demonstrate:

- Financial transparency

- Structured investment strategies

- Capacity to meet international compliance standards

will be better positioned to benefit from the new framework.

Conversely, informal, opaque, or opportunistic investment models are likely to face increasing regulatory friction.

This reflects a deliberate policy choice: to improve not only the volume, but also the quality of Vietnam’s outbound investment flows.

Reform Requires Systemic Alignment

Decree 103/2026/ND-CP marks a significant step forward in Vietnam’s outbound investment regulatory framework. It embodies a modern regulatory approach: reducing ex-ante barriers, strengthening ex-post supervision, and focusing on capital flow control.

However, for the Decree to achieve its intended impact, further steps are necessary:

- Harmonisation with foreign exchange, tax, and securities laws

- Clear inter-agency coordination mechanisms

- Digitalisation of reporting and compliance systems

Absent these developments, the Decree’s progressive features risk becoming new technical barriers in practice.

Ultimately, the key question is no longer whether outbound investment is permitted—but whether investors possess the capacity to navigate the system to completion.

By LawyerLinh Nguyen, Senior Partner

This article is based on legal analysis and practical experience, reflecting the professional views of the author/lawyer at the time of publication, and is not intended to constitute or substitute formal legal advice.

For specific legal matters, clients are encouraged to consult directly with our lawyers for tailored advice and strategically aligned legal solutions.

Read more other relevant articles:

- Tax Tips for Small Businesses in Vietnam to Avoid Mistakes (2026 Guide)

- Intellectual Property Compliance in Vietnam 2026: The Risks Businesses Do Not See

- Why Vietnam Is Asia’s Fastest Growing Investment Hub

- Foreign Company in Vietnam: Setup Guide for Investors 2026

- Vietnam Business Ideas 2026: Top Sectors and Legal Guide